USD, USDC, and USDT all carry the same dollar value. What they do not share is speed, flexibility, and reach, and those are the things that decide whether your earned income becomes usable income. Fiat is trusted but slow. USDC is the compliant digital dollar. USDT is the liquidity workhorse with regulatory fine print.

|

Factor |

USD (Bank Transfer) |

USDC |

USDT |

|

Typical payout speed |

1–5 business days |

Minutes |

Minutes |

|

Transfer fees |

Medium to high |

Low |

Low |

|

Value stability |

Stable |

Stable (USD-backed) |

Stable (USD-backed) |

|

Bank dependency |

High |

Low |

Low |

|

Cross-border transfers |

Slower |

Fast |

Fast |

|

Best for |

Traditional banking users |

Creators prioritizing speed and transparency |

Creators prioritizing broad platform support |

|

Control over funds |

Medium |

High |

High |

The USD vs USDC vs USDT question looks like a crypto detail. It is really a cash flow decision. The currency you choose for creator payouts shapes how fast you get paid, how much survives the trip, and how much control you keep over your own money. Here is the guide, with real numbers and a setup you can copy on a small channel this week.

Why Does Your Payout Currency Beat Your Revenue Size?

Revenue is a figure on a dashboard. Cash flow is money you can spend today. Those are two different things, and the gap between them is your payout currency.

Picture a creator clearing $1,500 a month. In one setup, that money is fast, stable, and in their wallet by the weekend. In another, it sits behind a bank hold, loses a slice to conversion, and shows up three weeks late. Same income on paper. A different life off it.

For small YouTube creators, this matters more than for the giants. When your income sits between $500 and $2,000, a three-week delay or a 4% fee is the difference between covering a shoot and skipping it. The big channels can absorb friction. You feel every dollar of it.

So before you compare fiat vs crypto payouts, hold onto the core idea: your creator income currency is part of your business model, not an afterthought at the cash-out screen.

USD Payouts: How Does Creator Money Move?

USD is fiat, the regular dollar that runs through banks. It is the default for YouTube payment methods, the Twitch payout system, and most brand deals in the US. It is trusted and universal. It is also the slowest and least flexible option a creator has.

The reason is the plumbing underneath. A bank payout does not travel in a straight line. A wire from a US sponsor to a creator abroad can hop through several correspondent banks, each taking a cut and adding a day. International wires usually settle in three to seven business days and can cost up to $50 per transfer, plus $15 to $30 in intermediary deductions you never see coming.

YouTube itself bakes in a wait. AdSense finalizes last month's income around the 7th to 10th, then pays between the 21st and 26th once you clear the $100 threshold. Money you made in January often reaches your bank in late February. That is a 30- to 60-day lag built into the system before a single fee applies.

Then there is conversion. When dollars convert to your local currency, some platforms use an internal rate 2 to 4% worse than the market. On a $10,000 month, that quietly removes $200 to $400 every cycle. PayPal can run a 2 to 4% transaction fee plus a 3 to 4% conversion spread, so a $5,000 payout at a 3.5% blended rate loses about $175 a month, or $2,100 a year.

USD has its strengths. Domestic rails like ACH in the US, SEPA in Europe, PIX in Brazil, and Zelle move fast and are low-cost inside their own regions. The trouble starts when money crosses a border, which is exactly what creator income does.

🎯 Practical tip: If you take USD, batch it. A creator paying five contractors with separate $40 wires loses up to $2,400 a year on fees alone. Consolidate into one larger transfer and pay your team from a faster rail instead.

USDC: The Compliance-First Digital Dollar

USDC is a stablecoin, a digital token pegged 1:1 to the US dollar. It moves at crypto speed but holds its value like cash, which is what makes stablecoin monetization work for day-to-day money. One USDC is built to always be worth one dollar.

- USDC is the one regulators and institutions tend to trust. Circle launched it in 2018 as a transparency-first coin. It publishes attestation reports every month, and roughly 98.9% of its reserves sit in short-dated US Treasuries and cash held at regulated institutions, with BNY Mellon as a primary custodian. You can see what backs it.

- That posture paid off in Europe. Under the EU's MiCA rules, Circle became the first global stablecoin issuer to get an Electronic Money Institution license, so USDC stays available and legal on regulated EU platforms. The wider US picture is moving in the same direction, with the GENIUS Act setting the first federal framework for stablecoins, including 1:1 backing and audits.

- USDC is not flawless. In March 2023, it briefly dropped to about $0.87 after Circle disclosed $3.3 billion parked at the failing Silicon Valley Bank. The peg snapped back within days once regulators stepped in, but it was a real reminder that even a careful stablecoin carries banking-partner risk.

🎯 Practical tip: If you want clean records for taxes, brand invoices, or a future business loan, USDC is the easier currency to defend. Its paper trail is built for the kind of creator who treats the channel like a company.

USDT: Liquidity King, With Fine Print

USDT, issued by Tether since 2014, is the most-used stablecoin on the planet. It holds around 59% of the entire stablecoin market and a market cap of nearly $187 billion, against roughly $75 billion for USDC. When people talk about crypto creator payments in emerging markets, they usually mean USDT.

Its strong suit is liquidity. USDT is accepted almost everywhere, trades on nearly every exchange, and moves cheaply on the Tron network. For a creator paying an editor in a country with slow banks or a shaky local currency, USDT is often the fastest dollar available. That reach is the real USDT vs USDC difference for working creators.

The fine print is where it gets serious. Tether has historically published attestations rather than full audits, though it hired KPMG in 2026 to change that. More importantly for some creators, USDT is not MiCA-compliant. Through late 2024 and early 2025, major EU platforms pulled it: Coinbase removed non-compliant coins first, then Crypto.com, Kraken, and then Binance delisted USDT spot pairs for EEA users on March 31, 2025. If you live in Europe and rely on regulated exchanges, that access gap is a practical problem, not a theoretical one.

USDT has also held its peg through stress, including the 2022 LUNA collapse, recovering each time. The risk is less about the dollar peg and more about regulatory ground shifting under your feet.

🎯 Practical tip: Match the coin to your region. If your team and your audience sit outside the EU, USDT's liquidity is hard to beat. If you operate inside Europe or want maximum compliance cover, lean USDC. Plenty of creators hold both.

Your Money, Your Currency

Cash out on your own terms, anytime, in 40+ currencies. Send your YouTube income to a bank, card, e-wallet, or crypto wallet, all from one hub. Try MilX, it is free to start and fully in your hands.

Banks vs Blockchains: The Speed Gap

The biggest difference between fiat and stablecoins is not the dollar amount. It is the clock.

- Bank rails keep office hours. They pause for weekends, holidays, and cut-off times. They route cross-border payments through a chain of intermediaries, and any one of them can hold your money for a compliance check. According to MilX data, payouts can sit frozen for weeks over account verifications that have nothing to do with your content quality.

- Blockchains do not sleep. A stablecoin transfer settles in minutes, any hour, any day, with no bank in the middle to slow it down or freeze it. A US creator paying an editor in the Philippines can have the money confirmed before a wire would have cleared its first hop.

- Speed has a catch worth knowing. The network you pick changes the cost. Sending USDT or USDC on Ethereum (ERC-20) can get expensive when the network is busy, while the Tron network (TRC-20) is far cheaper. One hard rule protects you here: always confirm the network before you send, because money sent to the wrong chain is gone for good.

🎯 Practical tip: Keep a small stablecoin balance as your fast-access pocket. When a sponsor pays late, or a bill lands early, a stablecoin transfer covers it the same day. Your slower USD payouts can settle in the background.

Earned Income is not the Same as Usable Income

This is the line that catches creators off guard. The money YouTube says you made is not the money you can spend. Between the two sits a gap made of waiting, fees, conversions, and holds.

Earned income is the dashboard number. Usable income is what survives the journey into your hands. A $2,000 month can become a $1,650 month after a 30-day wait, a conversion spread, and a withdrawal fee, and that is before anything goes wrong.

Sometimes a lot goes wrong. Some creators in countries without a US tax treaty lose 24% of their monthly income to default AdSense withholding, with no self-service fix. That is not a fee they chose. It is a structural leak tied to where they live, how their account is set up, and whether they are connected to the MCN

Your payout currency decides how wide that gap gets. Fiat, through international banks, widens it with delays and conversion costs. Stablecoins narrow it with speed and lower friction. The goal is simple: get usable income as close to earned income as you can.

Same Income, Three Different Financial Lives

Run one example through three currencies. Three creators, each clearing about $1,500 a month from a global audience.

- The first takes everything in USD through an international wire. The money is real but slow. It lands days late, loses a flat fee and a conversion spread, and a verification hold can stretch the wait into the next month. Reliable, rigid, and last to arrive.

- The second takes USDC. Payments settle in minutes, records stay clean for taxes and brand work, and the money is spendable the same day it moves. The trade-off is a network fee and the need to mind which chain they use.

- The third takes USDT for a team spread across countries with slow banking. The cash moves fast and cheaply on Tron, and contractors get paid without a banking headache. The watch-out is regulatory access if any of them sit inside the EU.

Same headline income. Three different bank balances, three different stress levels. The variable is creator cash flow currencies, not effort or talent.

Get Paid Before the Views Roll In

Stop waiting on the 21st of the month. Access up to six months of your future YouTube income today with MilX Active Funds, then put it straight into your next shoot, your editor, or your gear. Check if your channel qualifies for Active Funds

Why Creators Mix Fiat and Stablecoins

The creators who handle money well rarely pick one currency. They assign each one a job and let them work together.

This is not a fringe habit among crypto fans. According to MilX data drawn from thousands of monetized channels, more than 90% of creators who choose crypto payouts take them in stablecoins like USDT or USDC, not in volatile coins. They want crypto's speed for cash flow and the dollar's stability for their numbers.

A common split looks like this.

- USD stays the anchor for brand deals, big invoices, and anything that needs a bank paper trail.

- USDC handles fast, compliant payouts and clean records.

- USDT covers cross-border team payments where liquidity and low cost win. Each currency does what it is best at.

Mixing currencies also protects your scaling. A view-based payout has a soft ceiling, but how you move money does not have to cap your growth. When you can pay a global team instantly and reinvest the same day, you can take on bigger projects without a banking delay setting your pace. Currency flexibility is one of the levers that lets a small channel grow into a business.

🎯 Practical tip: Do not chase the perfect coin. Pick a primary stablecoin for speed, keep USD for formal payments, and add the second stablecoin only when a specific team or region needs it. Simple beats clever.

How to Optimize Your Payout Currencies: A Creator's Guide

Here is the practical part, scaled for a small channel. Work through it in order. None of it needs a finance degree.

- Map your money dates. For every income source, write the date you make the money and the date it lands. Pay your bills from the landing dates only. This kills most cash flow surprises.

- Match the currency to the job. USD for brand deals and formal invoices. A stablecoin for fast access and team pay. Decide this once, not at every cash-out.

- Pick your stablecoin by region. Inside the EU or need maximum compliance, choose USDC. Paying a team in countries with slow banks, USDT's liquidity is the practical pick.

- Always confirm the network. TRC-20 (Tron) is cheaper; ERC-20 (Ethereum) is more widely supported. Double-check the chain before you send, since a wrong-network transfer is lost for good.

- Watch the real fees, not the headline. Add up conversion spreads, intermediary deductions, and per-transfer charges. The cheapest method on paper is often the most expensive in practice.

- Keep a same-day pocket. Hold a small stablecoin balance for late sponsors and early bills. Let slower USD payouts settle behind it.

- Cover the timing gaps. When AdSense lags, or a sponsor pays on net-60, pull your future revenue forward instead of pausing your plan or selling something at a bad moment.

🎯 Reality check: You will not get all eight right at once. Lock in your money map and your currency-to-job rule first. The rest follows naturally.

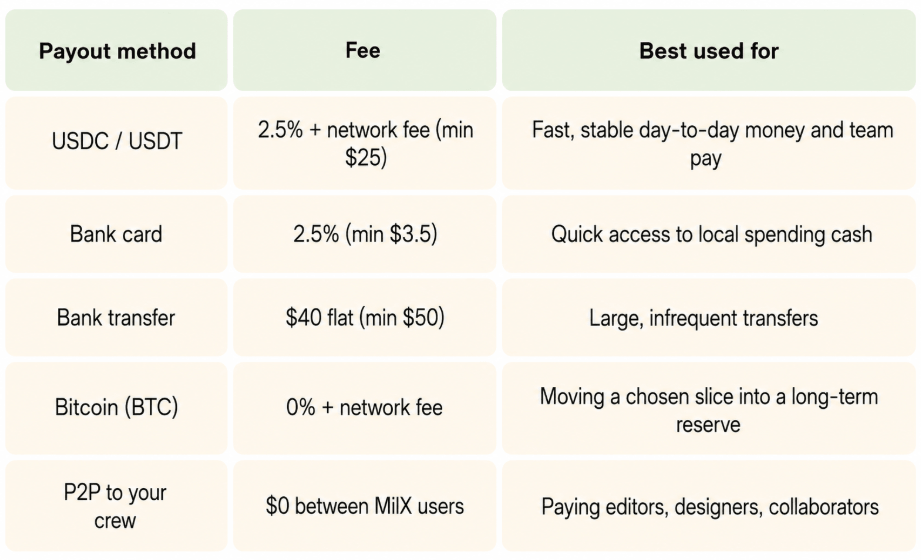

How MilX Handles Multi-Currency Payouts?

All of this only works if your money can flow the way you want. That is the gap MilX is built to close.

MilX lets you cash out across 40+ currencies and 10+ payout methods. You take fiat money where you need it and crypto where it makes sense, from the same dashboard. The fees are shown upfront, which matters when you are choosing between currencies.

Two details do real work. Stablecoin payouts keep your operating money predictable and let you choose the lowest-fee network. And Instant Payments deliver funds in under five minutes, so your cash flow stops depending on banking hours. You can also send free P2P transfers to anyone else on MilX, which removes the per-wire fees that punish creators with global teams.

👉 Want the deeper version? Read how creators move YouTube payments into crypto and explore the full list of 10+ ways to move your money.

What's the Way to Fund What's Next?

Choosing the right currency fixes how your money moves. Active Funds by MilX fixes when you get it. When a sponsor pays on net-60, or AdSense makes you wait a month, you can access up to six months of your future YouTube income upfront and put it straight into your next project.

With MilX, creators do not just get funded. They stay in control:

- Automatic repayment of 5% monthly from future income, so there is nothing to track.

- Low daily fees starting from just 0.33% per day.

- No credit checks and no score required.

- Cash out in 40+ currencies, including crypto.

- Choose from 10+ payout methods: bank, card, wallet, or crypto.

- Send free P2P transfers to editors, designers, and collaborators, fast and fee-free.

Whether you are scaling up, launching a new series, or just covering your next shoot, MilX gives you the room to move fast without looking over your shoulder. More than 5,000 creators already use it to stay ahead, without taking on debt. It has processed $500M+ in creator revenue, is an Official YouTube Partner, is regulated by Canada's Fintrac, and holds a 4.6 on Trustpilot, with no monthly subscription fees. Try MilX and see if your channel qualifies for Active Funds.