Plenty of YouTubers love Bitcoin. Almost none of them want their rent paid in it. That gap tells you something real about how a creator business handles money, and it has nothing to do with being scared of crypto.

This is the difference between income money and reserve money. Bitcoin for creators can work just fine as one and badly as the other. Get the two mixed up, and a great month can turn into a panic when the price moves. Get it right, and you build a creator treasury strategy that holds up when YouTube has a slow quarter.

Let's break down the actual logic, with real numbers, and end with a playbook you can run on a small channel this week.

Two Jobs, Two Completely Different Kinds of Money

Every business, from a corner bakery to a 50-person studio, splits its money into two buckets. One bucket pays the bills. The other sits in reserve.

- The first bucket is operating cash. Rent, your editor, the new mic, and the ad spend for next week. This money needs to be stable and ready. You want to know that $3,000 today is still $3,000 on Friday.

- The second bucket is the treasury. This is money you are not spending this month. It can take a few risks because it is playing a longer game. A reserve can ride out a bad week because you are not about to swipe it at the grocery store.

An income asset belongs in bucket one. It has to be steady, liquid, and boring. A treasury asset belongs in bucket two. It can be volatile if the long-term payoff is worth it. Bitcoin is the second kind of asset, which is exactly why creators rarely take it as operating income.

🎯 Tip for small channels: Before you think about crypto at all, draw the two buckets on paper. Write down your monthly costs in bucket one. Whatever is left after a comfortable safety margin is the only money that should ever go near a volatile asset.

Does Bitcoin Make a Brutal Paycheck?

Here is the problem with taking your salary in BTC. The price does not sit still long enough to be a paycheck.

Look at late 2025. From its October peak, Bitcoin lost roughly 30% of its value by the middle of November, according to Tesseract's treasury report. Imagine your brand deals landed as BTC in early October. Almost a third of it could vanish before you paid December rent, while the views that money came from never changed.

The numbers back this up beyond one bad month. On average, Bitcoin's 60-day volatility at 1.58%, against roughly 1.2% for gold and just 0.5% to 1% for most national currencies. Even after years of maturing, Bitcoin still swings far harder than the dollar your costs are priced in.

Big companies feel this, too. Tesla booked more than $140 million in losses on its Bitcoin during the 2022 downturn. If a firm that size takes that kind of hit on a reserve position, a solo creator should never sit their grocery money on the same rollercoaster.

This is the heart of the Bitcoin volatility income problem. Your bills are fixed. Bitcoin is not. Pairing a fixed cost with a wildly moving asset is how creators end up selling at the worst possible moment, just to make payroll for one editor.

🎯 Tip: A simple rule keeps you safe. Never hold money you need within 90 days in any asset that can drop 30% in a month. Short-horizon money stays stable. Long-horizon money can wander.

How to Structure Creator Income?

Walk into the back office of most working creators, and the setup looks the same.

For day-to-day money, that means dollars or dollar-pegged stablecoins like USDC and USDT. A stablecoin is a digital token tied 1:1 to a currency such as the US dollar. It moves at the speed of crypto but holds its value like cash, so it solves the stablecoin vs Bitcoin payments question before it starts. You get fast, borderless payouts without the price doing somersaults overnight.

This is not a fringe habit. According to MilX data drawn from thousands of monetized channels, more than 90% of creators who choose crypto payouts take them in stablecoins like USDT or USDC, not in Bitcoin. The crypto-friendly crowd already votes with its wallet. They want the rails of crypto for their YouTube crypto earnings and the stability of the dollar for their cash flow.

The reason is plain. When you pay an editor in Manila or buy gear priced in dollars, you need the amount to be exact. A stablecoin keeps crypto payouts on YouTube predictable. Bitcoin cannot promise that this week.

🎯 Tip for small creators: If you want crypto in your life, start by routing payouts into USDC, not BTC. You get the lower fees and the global reach, and your numbers stay readable. You can always move a slice into Bitcoin later, on your own terms.

Your Money, Your Way

Get paid on your own terms, anytime, in 40+ currencies. Send your YouTube income to a bank, card, e-wallet, or crypto wallet, all from one hub. Try MilX, it is free to start and fully in your hands.

Operating Cash vs Treasury Allocation: The Line That Protects You

The line between these two buckets is the most useful thing a creator can draw. On one side sits operating cash, the money that runs the business. On the other side, treasury allocation, the money that grows the business over the years.

- Operating cash answers a daily question: Can I pay for what I need right now? It has to be liquid. You should be able to spend it in minutes without watching a chart.

- Treasury money answers a different question: What is my surplus doing while I sleep? This is where your financial strategy with crypto can make sense. A reserve can hold an asset that swings because it is not on call.

The mistake that wrecks creators is funding bucket one with bucket two's risk profile. When your rent money lives in Bitcoin, every dip becomes a crisis. When only your surplus lives there, a dip is just a Tuesday. Same asset, completely different stress, decided entirely by which bucket it sits in.

🎯 Tip: Keep a written floor. Decide on the cash cushion you never touch, say three months of costs, and hold it in dollars or stablecoins. The rest os to invest. Where exactly, is up to you.

When Bitcoin Belongs in the Reserve?

None of this means Bitcoin is bad. As a long-term reserve, it has a genuine case, which is why so many companies now hold it.

Start with scarcity. Bitcoin's supply is capped at 21 million coins, by design, which makes it resistant to the inflation that eats cash. Over the last decade, the Argentine peso lost about 99% of its value against the dollar, while Bitcoin rose nearly 16,000%. For anyone whose local currency leaks value every year, a hard-capped reserve asset is worth a look.

The institutions agree carefully. Imagine nearly 200 companies now hold Bitcoin as a treasury asset, and businesses and governments across 32 countries hold around 8% of all the Bitcoin in circulation. Corporate holdings more than doubled in 2025, with over $100 billion of BTC sitting on balance sheets. This is the BTC income vs savings split in action: nobody runs payroll in it, plenty of them park savings in it.

Notice the word these reports keep using. Balance sheet. Not a paycheck. Bitcoin shows up as a store of value, a reserve line, a long bet on scarcity. It earns its spot in the treasury precisely because it is too jumpy for the checking account.

🎯 Tip: If you decide to hold some BTC as a reserve, do not size it like a gambler. Allocating a small slice of a portfolio to Bitcoin, around 4%, and rebalancing every quarter, has historically captured upside while keeping the swings survivable. Small and steady beats all-in.

Get Paid Before the Views Roll In

Stop waiting on the 21st of the month. Access up to six months of your future YouTube income today with MilX Active Funds, then put it straight into your next shoot, your editor, or your gear. Check if your channel qualifies for Active Funds

When the Coin Drops? Bitcoin's Most Damaging Scandals

Bitcoin was built on the promise of trustless finance: no banks, no intermediaries, no single point of failure.

In practice, the biggest failures came not from the protocol itself, but from the humans around it: exchange founders, fund managers, state-sponsored hackers, and outright con artists.

These are the cases that shook the market, wiped billions from portfolios, and left hundreds of thousands of users with nothing.

Silk Road: A Billion-Dollar Drug Market (2011–2013)

Silk Road was the first major darknet marketplace where Bitcoin served as the sole currency – anonymous, irreversible, bank-free. Drugs, weapons, and forged documents worth billions of dollars changed hands through the platform.

The FBI shut it down in 2013 and arrested founder Ross Ulbricht, who received a life sentence.

Mt. Gox: The Heist That Defined an Era (2011–2014)

At its peak, Mt. Gox handled over 70% of all global Bitcoin transactions. By February 2014, it was gone. Russian hackers had been systematically draining the exchange since as early as 2011, exploiting poorly secured private keys and virtually nonexistent internal controls.

By the time the collapse became public, 850,000 BTC had vanished: 740,000 belonging to customers, 100,000 to the company itself. At 2014 prices, the loss was roughly $460 million.

Bitfinex: $72 Million Stolen (2016)

In August 2016, hackers broke into Hong Kong-based exchange Bitfinex and made off with approximately 120,000 BTC – worth around $72 million at the time.

The exchange survived by issuing debt tokens to affected users, effectively distributing the loss across its entire customer base.

PlusToken: Asia's Largest Bitcoin Ponzi Scheme (2018–2020)

PlusToken was a Chinese Ponzi scheme that collected roughly $2 billion worth of cryptocurrency – including at least 45,000 Bitcoin – from millions of victims by promising returns of 10–30% per month. Once the scam collapsed, the fraudsters didn't just disappear with the money: they systematically laundered it through mixers, peel chains, and over-the-counter brokers on the Huobi exchange, converting stolen Bitcoin into Tether to obscure the trail.

FTX: The Exchange That Spent Its Customers' Money (2022)

FTX was valued at $32 billion in early 2022. By November, it was bankrupt. Founder Sam Bankman-Fried had been routing customer deposits to Alameda Research, his trading firm, to cover losses and fund personal investments – including political donations and real estate.

When a leaked balance sheet triggered a bank run, FTX could not meet withdrawals. Bankruptcy filings revealed that almost $9 billion in customer assets were missing or misused. Bankman-Fried was arrested, tried, and convicted on seven counts of fraud and conspiracy. He was sentenced to 25 years in prison.

The collapse triggered a market-wide crash, with Bitcoin falling from around $21,000 to below $16,000 in a matter of days.

Bitcoin Fraud: How the Money Gets Stolen?

Bitcoin attracts fraudsters for several reasons: transactions are irreversible, there are no international borders, and with the right laundering techniques, tracing funds is difficult. Here are the most common schemes.

QR Code Disguised as KYC – A New and Dangerous Scheme

One of the newest schemes works like this: the victim wants to cash out Bitcoin through an unverified exchange point or contractor.

During the verification stage, they are sent a QR code supposedly for completing KYC (Know Your Customer – a standard identity verification procedure).

In reality, the QR code is a payment link. One scan, and the funds go straight to the fraudster's wallet. There is no way to get them back.

Why this is dangerous:

- It looks like a legitimate procedure that licensed exchanges genuinely require.

- Once confirmed, the transaction is irreversible: neither a bank nor the police can stop the transfer.

- Fraudsters move the funds onward within 24–48 hours, making tracing even harder.

The rule: no legitimate KYC process requires scanning a QR code that initiates a payment. KYC is identity verification, not a money transfer.

Bitcoin ATMs: $333 Million Stolen in 2025

The FBI received over 13,400 complaints about crypto ATM fraud in 2025, with total losses of $388 million. The scheme is straightforward: the victim receives a call (often using a deepfake voice), the caller poses as a bank or government agency, and claims the account has been frozen.

To "rescue" the funds, the victim is told to withdraw cash and deposit it at a Bitcoin ATM – by scanning a QR code on the screen (which belongs to the fraudster).

AI Deepfakes to Bypass KYC on Exchanges

Fraudsters have learned to bypass identity verification on crypto exchanges: generative AI produces realistic counterfeit documents (passports, driver's licenses) that successfully pass automated KYC checks. This allows accounts to be opened under stolen or fabricated identities – for money laundering or to evade account blocks.

Pig Butchering

A long-con trust scheme: the fraudster spends months building a relationship with the victim (romantic or friendly – on social media or in messengers), then recommends a "proven" Bitcoin investment platform.

The victim invests more and more, watching "growing profits" on a fake dashboard. When they try to withdraw, the account is frozen, or they are asked to pay a "withdrawal fee." The money disappears along with the "friend."

Laundering Through Mixers and Conversion

After a theft, Bitcoin rarely stays in its original form. Fraudsters convert it into harder-to-trace coins (Monero, ETH), run it through mixers (services that blend transactions from multiple users), and, before cashing out to fiat, shift it into stablecoins (USDT, USDC). The window between theft and withdrawal has shrunk to 48 hours.

Why Bitcoin Is Hard to Trace?

A popular myth: Bitcoin is anonymous. The reality is more complicated.

Bitcoin is pseudonymous, not anonymous: every transaction is recorded on a public blockchain, but wallet addresses are not automatically linked to real names. If a fraudster never exposed their address anywhere – never went through KYC, never traded on a regulated exchange – identifying them is extremely difficult.

In practice:

- Investigators can follow the chain of transactions, but identifying a person requires a point where the crypto intersected with a real identity (an exchange, ATM, or broker).

- The use of mixers, privacy coins, and unregulated P2P exchanges significantly complicates investigations.

- Transactions are irreversible: even if a fraudster is caught, recovering the funds is technically impossible without their cooperation.

This is why Bitcoin remains the tool of choice for ransomware operators, drug trafficking, and international fraud.

How to Protect Yourself

- Only cash out cryptocurrency through licensed, verified platforms with a public track record and regulatory approval.

- Never scan QR codes from strangers or unverified sources in a crypto context – even if it's presented as "KYC."

- Always verify the wallet address manually before any transfer.

- If someone calls claiming to be from your bank and asks you to do anything with a crypto account – hang up and call the bank yourself using the official number.

- Remember: Bitcoin transactions are irreversible. There is no way to undo a mistake or a fraud.

Multi-Currency Payout Logic: How Can You Move Money in Crypto?

This two-bucket system only works if your money can flow the way you want it to. That is the gap MilX is built to close for creator crypto monetization.

MilX lets you cash out YouTube earnings in 40+ currencies via 10+ payout methods. You can take fiat money where you need it and crypto where it makes sense, from the same dashboard. For Web3 creator payments, that flexibility is the whole point: stablecoins for cash flow, Bitcoin for the reserve, your call.

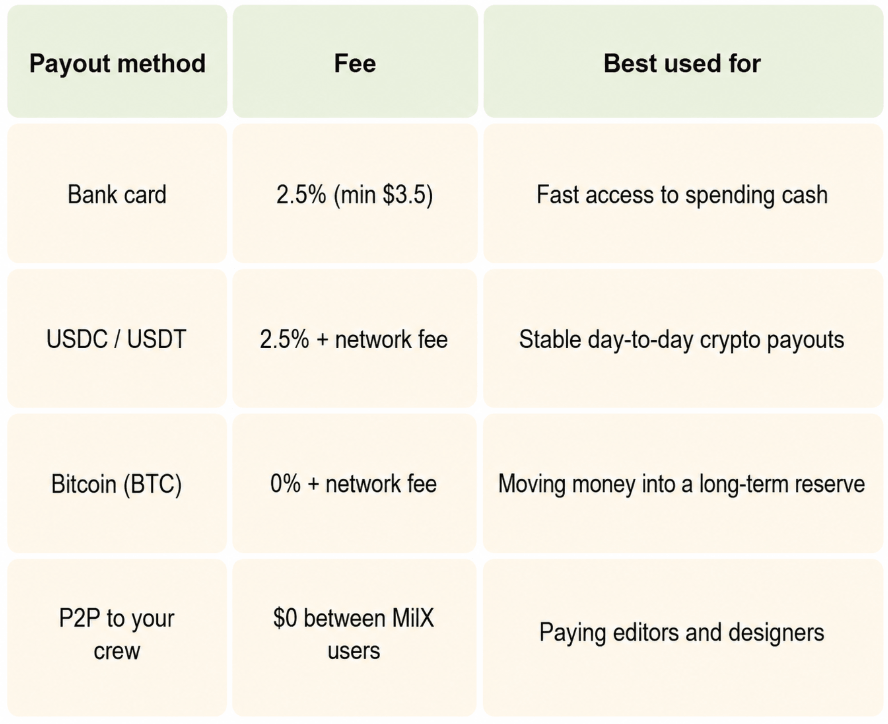

The fees are laid out plainly, which matters when you are choosing between buckets:

Two details do real work here. Stablecoin payouts keep your operating money predictable. And because BTC withdrawals carry no MilX fee on top of the network cost, moving a chosen slice into your reserve stays cheap when you decide the timing is right.

👉 Want the deeper version? Read how creators move YouTube payments into crypto.

Your Creator Treasury Playbook

Here is the practical part, scaled for a small channel. Work through it in order. You can start this week, and none of it needs a finance degree.

- Split your money into two buckets. Operating cash for everything due in the next 90 days. Reserve for everything beyond that. Write the line down so it is real.

- Take income from something stable. Route payouts into dollars or USDC, not BTC. Your cash flow should never depend on a chart.

- Set a cash floor and hold it. Three months of costs, kept in stable money, untouched. This is the cushion that turns a crisis into a shrug.

- Define your surplus. It’s safer to invest money in volatile asset only above the floor. If there is no surplus this month, that is your answer: no BTC this month.

- Size your Bitcoin reserve small. A modest slice of surplus, rebalanced quarterly, captures upside without betting the business.

- Cover the timing gaps. When AdSense lags, access your future YouTube revenue, so slow payouts never force you to sell a reserve asset at a bad price.

🎯 Lock in the two buckets and the cash floor first. The Bitcoin part is the last step, not the first.

The Smarter Way to Fund What's Next

Building the two-bucket system is the strategy. Keeping your money moving is the part MilX helps to handle.

When a sponsor pays on net-60, or AdSense makes you wait, you do not have to dip into your reserve. With MilX Active Funds, you can access up to six months of your future YouTube income upfront and put it straight into your next project. No credit checks. No score required.

- Automatic repayment of 5% monthly from future income, so there is nothing to track.

- Low daily fees starting from just 0.33% per day.

- Cash out in 40+ currencies, including crypto.

- 10+ payout methods: bank, card, wallet, or crypto.

- Free P2P transfers to pay editors, designers, and collaborators, fast and fee-free.

More than 5,000 creators already use MilX. Whether you are launching a new series, covering a shoot, or hiring your first editor, it gives you room to move fast. Try MilX and put your creator income to work.

The takeaway is simple. Bitcoin is not a salary. It is a balance sheet asset. Pay yourself in stable money, keep a cash floor, and let Bitcoin sit in the reserve where its swings can do some good instead of some damage.